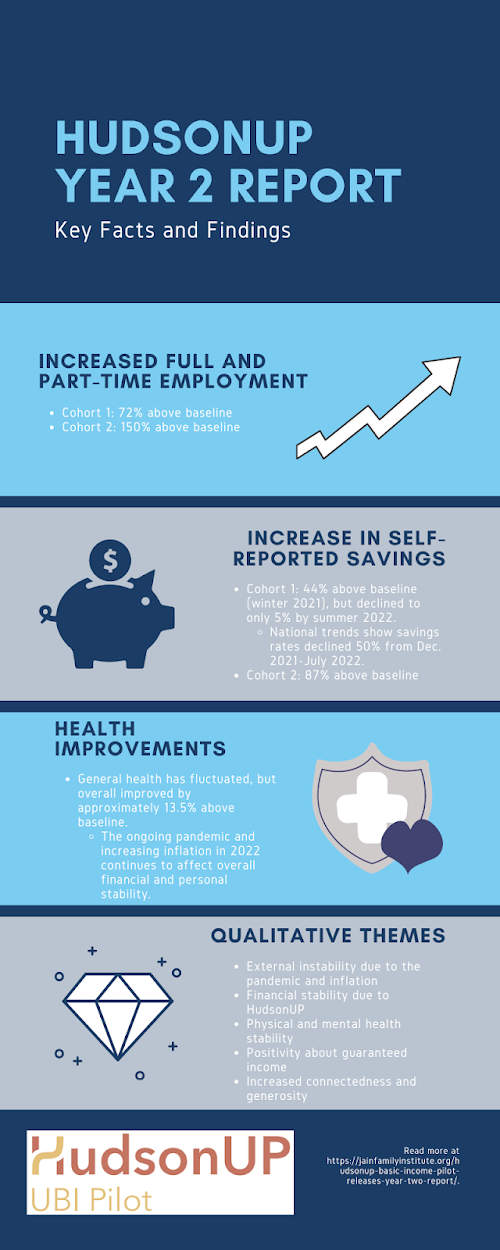

The HudsonUP Basic Income (BI) pilot’s second year wrapped up in the Fall of 2022, which includes 75 individuals over two cohorts. Our lab collected data bi-annually through surveys and interviews with willing participants. In Fall 2022 a third cohort of 53 participants was added, bringing the pilot’s total number to 128 participants. HudsonUP’s unique 5-year length allows a deeper look into the effects of BI on individuals over time. The pilot encompasses a diverse set of Hudson, NY residents, and supports approximately 2% of all Hudson residents, nearly 5% of Hudson households, and 9% of residents living in poverty. Quantitative data from the two cohorts shows that employment rates are steadily increasing above baseline, rising 72% in cohort one, and 150% in cohort two. Along with this, participants increased their savings and made steady improvements to their health. Overall, participants experienced positive c...

Comments

Post a Comment