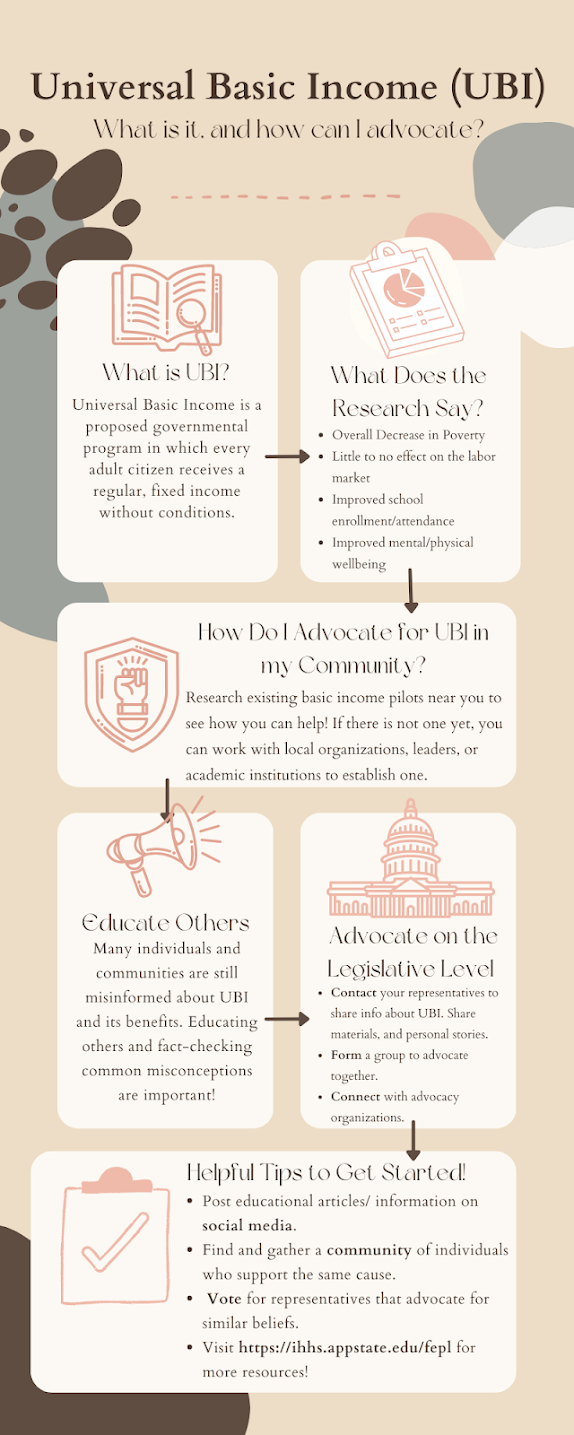

What is Universal Basic Income?

In Her Hands is a guaranteed income initiative focused on putting a solution to financial insecurity directly in the hands of women in Georgia. Due to historical and current inequalities in income and institutional supports, Black women are among the most likely group to experience cash shortfalls that make covering basic needs difficult. This is the result of pervasive economic disparities that have the sharpest impact on women, communities of color, and people who live at the intersection of the two.

In Her Hands, formed through direct community input, will provide an average of $850 per month for 24 months to 650 women in three communities in Georgia. This $13 million initiative, powered by a partnership with the GRO Fund and GiveDirectly, is already one of the largest guaranteed income programs in the South, a region where women of color face significant structural barriers to economic security and wealth-building. Direct, no-strings-attached cash allows individuals and families to invest in what they need— from providing for basic needs, to keeping a roof over their heads, to paying for medical care, to investing in their family and future — and maintain agency over their lives while doing so.

The first location to participate in the initiative was in Atlanta’s Old Fourth Ward (O4W), the neighborhood where Dr. Martin Luther King, Jr. grew up and later preached about guaranteed income. The second location to participate is rural Southwest Georgia’s Clay-Randolph-Terrell (SW GA) country cluster while the third location is the suburban City of College Park.

Community-based organizations, policy advocates, and government leaders across the U.S. and other countries are increasingly pointing to guaranteed income as a policy that can make a significant impact in people’s lives. We hope to add to this conversation by studying how guaranteed income can particularly benefit Black women — a population in Georgia that has historically faced disproportionate structural barriers at the intersection of both gender and racial wealth gaps.

The research component of this project is led by Dr. Leah Hamilton at Appalachian State University and is specifically designed to help us understand the mechanisms by which cash can improve women’s lives and wellbeing.

Site 1 and 2 Baseline Findings

On the US Consumer Financial Protection Bureau (CFPB) Financial well-being Scale, which is a standardized number between 0 and 100 that represents the respondent’s underlying level of financial well-being, participants overall reported a 45.29. Regarding food security in the previous six months, 75.5% of participants reported that the food they bought did not last, 65.5% reported that they could not afford to eat balanced meals, 39.9% of participants reported skipping or cutting the size of their meals, and 39.6% of participants reported being hungry not not eating because there was not enough money for food.

Participants overall had a wide range of goals over the next two years including catching up or getting ahead on bills (56.7%), building emergency savings (28.4%), reducing debt (27.6%), buying or improving their house (22.2%), improving their credit score (20.4%), and starting or growing a small business (16.0%). To assess life satisfaction and optimism, participants were asked to “Please imagine a ladder with steps numbered from zero at the bottom to 10 at the top. The top of the ladder represents the best possible life for you and the bottom of the ladder represents the worst possible life for you.” Overall, they reported that at the time, they were at about a 5.27 on the ladder and predicted that they would be at an 8.35 on the ladder five years from now. For reference, previous research has found a roughly one point gap between current life satisfaction and optimism among low-income African Americans (Graham et al., 2022).

Please stay tuned as we track the experiences of In Her Hands participants and how an unconditional guaranteed income impacts the lives of recipients, their families, and the communities around them.

To follow our journey:

Comments

Post a Comment